A recent Africa’s Pulse report found that COVID-19 is likely to drive Sub-Saharan Africa into its first recession in 25 years, with economic growth in the region declining from 2.4 % in 2019 to between -2.1 % and -5.1 % in 2020. The decline will be primarily due to large contractions in South Africa, Nigeria, and Angola whose economies have existing structural issues and are overly reliant on exports. Growth is expected to recover to positive levels by 2021, although it will remain below the levels of economic growth in 2018 and 2019.

While COVID-19 is a global challenge, Africa is especially vulnerable to the associated economic disruptions, since 90% of people work in the informal sector. Projections suggest that the 2020 recession could push 80 million Africans into extreme poverty, whose suffering will be compounded by a looming food security crisis due to agriculture production decreasing from between 2.6% and 7%.

The United Nations Economic Commission for Africa (ECA) has said that African cities will be hardest hit by COVID-19. Indeed, African cities are also where the virus is expected to be most pervasive since they are home to 600 million people, and account for more than 50% of the region’s Gross Domestic Product (GDP). It is also in African cities where pressures relating to fiscal shortages, increased poverty, and food shortages are likely to converge to increase the risks of social unrest and violent conflict.

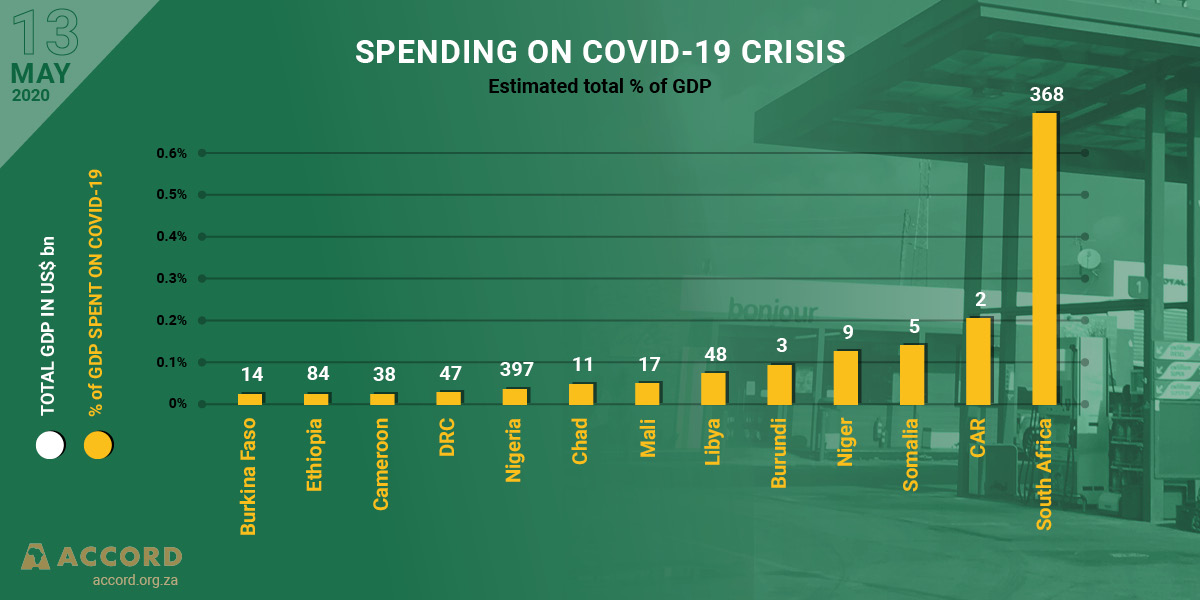

A number of African countries have introduced fiscal and monetary policies that have been designed to enable some social protection against the negative effects of COVID-19 containment measures. The World Bank categorizes these policies as either social assistance, social insurance, or labour market measures. In Africa, countries have on average budgeted a modest 1.07% of their GDP to these types of COVID-19 safety net policies. However, there is still a significant gap between what has been raised and the US$ 114 billion that these policies are expected to cost in 2020. For these policies to be effective, they will need to be customized to the structural features of the region, namely:

- The precariousness of most jobs in the region;

- The importance of small and medium-sized enterprises that make up 90% of business units and are the drivers of growth in the region;

- The ineffectiveness of monetary stimulus as a result of reduced labour supply and business closures, and in the recovery phase due to weak monetary transmission in countries with underdeveloped financial markets;

- The need to strengthen health systems; and

- Minimizing disruptions to domestic and international food supply chains.

These COVID-19 social net policies can also be appreciated for their ability to disrupt the relationship between poverty and conflict. This relationship becomes mutually reinforcing when the reduction of domestic economic activity creates incentives for social unrest and conflict, which in turn reinforces low levels of domestic economic activity. Across Africa, violence and social unrest could further erode confidence in already weak governments and vulnerable economies, creating a poverty-conflict trap, or a negative mutually re-enforcing downward spiral. While the initial cost may be high, and policies may be difficult to implement, the social-net policies introduced thus far should increase the resilience of those countries to withstand some of these negative effects, and allow the economy to start to recover.